Ancillary cannabis companies (those that are not plant touching businesses) offer investors a chance to buy cannabis “pick and shovel” plays. “Picks and shovels” is an old gold mining reference pointing to those that sold the picks, shovels and other supplies to the gold miners, considered a less riskier way to generate wealth compared to the gold miners who mostly relied on luck. All the gold miners needed supplies, but most didn’t earn a living off of gold.

There are many advantages to investing in the cannabis pick and shovel plays:

- Non-plant touching companies can list on the major U.S. exchanges thus having stock liquidity and access to capital and normal banking

- Institutional investors can invest in them

- They make money no matter how federal legislation plays out

- Many of them sell to the legal and illicit markets

- They can deduct normal expenses which plant touching businesses can’t

Two relatively unknown ancillary cannabis plays are Agrify and urban-gro, two companies that focus on the hardware, engineering and software that helps optimize cannabis grow facilities. I recommend you review each of their investor presentations or page (Agrify doesn’t have an investor deck) to understand their businesses fully.

For my analysis of the stocks, I’m specifically focusing on stock fundamentals.

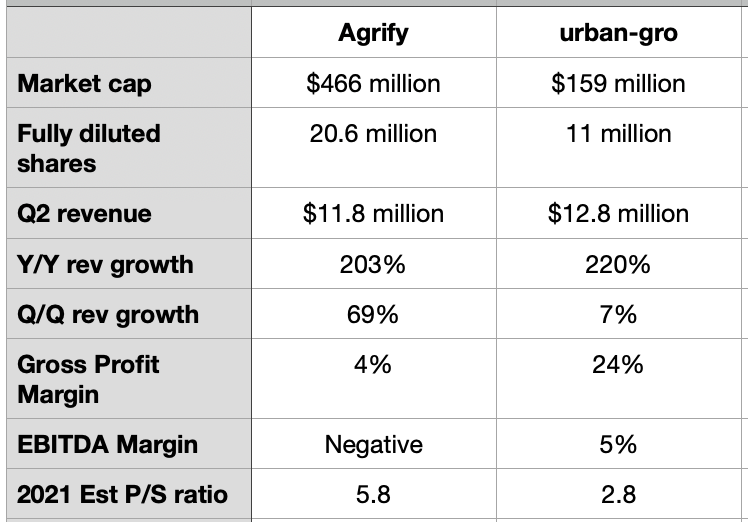

Current Fundamentals

A few things stand out in urban-gross favor:

- While trading at 1/3 the market cap, urban-gro had $1 million more in revenue in the second quarter. This puts urban-gro at a significant discount at 2.8x estimated 2022 sales compared to Agrify’s 5.8 multiple. urban-gro’s stock would have to appreciate 107% just to catch up to Agrify’s multiple.

- urban-gro is far more profitable with a significantly better gross and EBITDA margins and urban-gro generated a $200,000 income from operations in Q2.

Future revenue growth

Agrify did have the better quarter-over-quarter revenue growth and significantly higher bookings and backlogs. urban-gro had a backlog of $27.9 million at the end of Q2 2021 an increase of $12.7 million, or 84% from the end of Q1 2021. Agrify new bookings were $30.7 million for Q2 2021 and total backlog increased to $101.1 million from $82.2 million at the end of Q1 2021. While urban-gro had more revenue in the most recent quarter, Agrify looks to have a significant edge on new bookings and backlog of revenue.

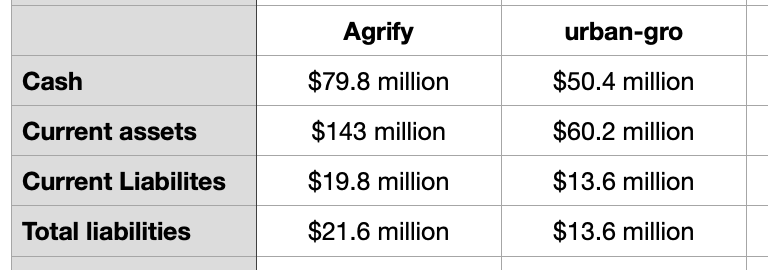

Balance Sheet

Both companies have very solid balance sheets, plenty of cash and current assets to pay current liabilities (bill due with 12 months). Agrify has very little debt and urban-gro has no debt. urban-gro has half the full-diluted share count, but Agrify has more than twice the current assets. Both balance sheets are very strong, but Agrify does have more shareholder equity.

In conculsion

From a fundamental standpoint, it is hard to say which stock is better than the other – urban-gro has more current quarterly revenue, but Agrify clearly has more contracts signed for future growth. The question potential investors should ask is, should Agrify trade at more than twice the price/sales ratio when urban-gro is much more profitable? Investors should feel comfortable investing in either company if the share price hits their target window. It’s up to each investor to decide if they prefer a more profitable, yet smaller company like urban-gro, or Agrify that has lesser profitabilty margins but has more future revenue booked with more shareholder equity built up.

– Part 3: Hollister Biosciences")