Organigram Holdings Inc. (NASDAQ: OGI) (TSX: OGI), the parent company of Organigram Inc. (together, the “Company” or “Organigram”), a leading licensed producer of cannabis, announced its results for the second quarter ended February 28, 2021 (“Q2 2021”).

“Although Q2 2021 results were challenged by industry dynamics, COVID-19 and staffing limitations at our facility, we believe there are excellent prospects ahead for the industry, Organigram and our shareholders,” said Greg Engel, Chief Executive Officer of Organigram. “Nearer term, we are currently tracking to generate higher revenue in Q3 2021 as our new product portfolio continues to gain traction and we become better staffed to fulfill demand. Our recent acquisition of The Edibles and Infusions Corporation positions us to generate revenue from the largest single category of edibles, soft chews or gummies. We also see the potential for meaningful gross margin improvement over time as we revitalize our dried flower portfolio with new Edison and Indi strains and execute on a number of opportunities including the refinement of our cultivation, post harvesting and packaging processes. Longer term, we are extremely excited about developing innovative and appealing products to consumers in collaboration with BAT. All of this is made possible and supported by strong liquidity and a balance sheet that is largely debt-free.”

| nm – not meaningful |

| * Adjusted gross margin, adjusted gross margin % and adjusted EBITDA are non-IFRS financial measures not defined by and do not have any standardized meaning under IFRS; please refer to the Company’s Q2 2021 MD&A for definitions and a reconciliation to IFRS. |

| ** Sales and marketing and general and administrative expenses (“SG&A”) excluding non-cash share-based compensation. |

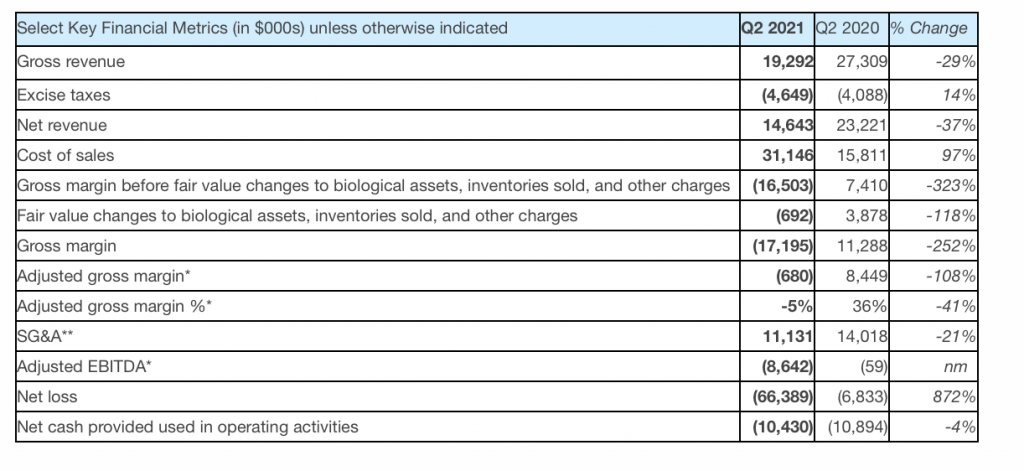

Key Financial Results for the Second Quarter Fiscal 2021

- Net revenue:

- Q2 2021 net revenue decreased from Q2 2020 primarily due to significantly lower wholesale revenue and a lower average selling price in Q2 2021. The higher wholesale revenues during Q2 2020 were opportunistic in nature, primarily sales to a single licensed producer.

- Q2 2021 net revenue was also lower due to missed sales opportunities, as certain employees tested positive for COVID-19 which resulted in a significant number of facility staff having to isolate.

- The Company was unable to fulfill certain demand for its products totaling approximately $7 million in Q2 2021 due to production and processing constraints.

- Q2 2021 revenue was also negatively impacted by certain provincial boards aiming to manage lower levels of inventory such as Alberta.

- Gross revenue:

- Q2 2021 gross revenue decreased from Q2 2020 largely due to similar factors impacting net revenue described above.

- Q2 2021 gross revenue decreased from Q2 2020 largely due to similar factors impacting net revenue described above.

- Cost of sales:

- Higher cost of sales in Q2 2021 was primarily due to higher Q2 2021 inventory provisions, a higher cost of production, and a charge related to unabsorbed fixed overhead as a result of lower production volumes in Q2 2021.

- Higher cost of sales in Q2 2021 was primarily due to higher Q2 2021 inventory provisions, a higher cost of production, and a charge related to unabsorbed fixed overhead as a result of lower production volumes in Q2 2021.

- Gross margin before fair value changes to biological assets, inventories sold, and other charges:

- Negative and lower gross margin in Q2 2021 was largely due to lower net revenue and higher cost of sales as described above.

- Negative and lower gross margin in Q2 2021 was largely due to lower net revenue and higher cost of sales as described above.

- Gross margin:

- Q2 2021 gross margin was negative compared to positive Q2 2020 gross margin largely due to negative Q2 2021 gross margin before fair value changes to biological assets, inventories sold, and other charges as described above as well as net non-cash negative fair value changes to biological assets and inventories sold in Q2 2021 versus positive changes in Q2 2020.

- Q2 2021 gross margin was negative compared to positive Q2 2020 gross margin largely due to negative Q2 2021 gross margin before fair value changes to biological assets, inventories sold, and other charges as described above as well as net non-cash negative fair value changes to biological assets and inventories sold in Q2 2021 versus positive changes in Q2 2020.

- Adjusted gross margin3:

- Q2 2021 adjusted gross margin was negative compared to positive Q2 2020 gross margin primarily due to lower net revenue as described above and value segment offerings comprising a larger proportion of total revenue in Q2 2021.

- Q2 2021 adjusted gross margin was negative compared to positive Q2 2020 gross margin primarily due to lower net revenue as described above and value segment offerings comprising a larger proportion of total revenue in Q2 2021.

- Selling, general & administrative (SG&A) expenses:

- Q2 2021 SG&A decreased from Q2 2020 largely due to higher professional and consulting fees in Q2 2020 related to project specific work, including the launch of Rec 2.0 products.

- Q2 2021 SG&A decreased from Q2 2020 largely due to higher professional and consulting fees in Q2 2020 related to project specific work, including the launch of Rec 2.0 products.

- Adjusted EBITDA4:

- Q2 2021 negative adjusted EBITDA declined from positive adjusted EBITDA in Q2 2020 largely due to lower adjusted gross margin in Q2 2021 as discussed above.

- Q2 2021 negative adjusted EBITDA declined from positive adjusted EBITDA in Q2 2020 largely due to lower adjusted gross margin in Q2 2021 as discussed above.

- Net loss:

- Q2 2021 net loss was greater than the Q2 2020 net loss largely due to the negative change in the fair value of the derivative warrant liabilities and the negative gross margin in Q2 2021.

- Q2 2021 net loss was greater than the Q2 2020 net loss largely due to the negative change in the fair value of the derivative warrant liabilities and the negative gross margin in Q2 2021.

- Net cash used in operating activities:

- Q2 2021 net cash used in operating activities remained stable relative to Q2 2020, despite lower gross margin in Q2 2021, largely due to the prior period’s increase in working capital assets as the Company continued to scale operations ahead of Rec 2.0 launches.

Canadian Adult-Use Recreational Market

Rec 1.0

Higher Margin Edison and Indi Dried Flower Strains

- In late December 2020, the Company launched three new Edison Indica strains namely Black Cherry Punch, Ice Cream Cake (I.C.C.) and Slurricane. The Company expects to launch additional high THC strains under the Edison brand in Q3 2021.

- Subsequent to quarter-end in late March, Organigram launched the Black Cherry Punch, I.C.C. and Slurricane strains in a package of three 0.5g pre-rolls. Also, in late March, the Company introduced Indi, one of Canada’s only cannabis brands dedicated exclusively to indica cultivars. Skyway Kush is the first strain in the Company’s Indi portfolio and currently offers THC in the range of 20% to 23%.

Value segment offerings

- In Q1 2021, Organigram expanded its strong value portfolio with the launch of SHRED, a high quality, high potency and affordable dried flower that is pre-shredded for consumer convenience. SHRED offers three pre-milled varieties, all with THC of 18% or more. It is made from whole flower, does not contain any shake or trim and is milled to the same specifications as the Company’s pre-roll products. SHRED is currently Organigram’s most affordable option (on a per gram basis).

- In March 2021, the Company announced that it expanded the successful SHRED brand with the introduction of a Jar of Joints, a convenient jar of 14 x 0.5g pre-rolls in SHRED’s Tropic Thunder.

Rec 2.0

Cannabis-Infused Chocolates

- The Company’s chocolate portfolio consists of Trailblazer SNAX, a value-priced chocolate bar and Edison Bytes truffles. Organigram’s investment in state-of-the art chocolate equipment means that each section of the SNAX bar is filled separately, allowing for higher accuracy of infusion. In Q2 2021, the Company launched milk chocolate, a new flavour of Trailblazer SNAX, and the Company has plans to introduce further Edison Bytes products in the next few quarters.

Vapes

- Organigram expects to launch new vape products with higher THC concentrations in Q3 2021, including an Edison + Feather disposable vape pen at a competitive price point as well as a 1g Edison cartridge for the 510 vaporizer, both of which will be based on the Company’s popular Limelight strain.

Research and Product Development

- Organigram continues to focus on innovation and research and product development. Examples of this hallmark of the Company include its nanoemulsification technology (described above) as well as its investment in biosynthesis through Hyasynth (see Hyasynth section of the Q2 2021 MD&A) and most significantly, its recent March 11, 2021 announcement of the Product Development Collaboration (“PDC”) with BAT.

- The R&D laboratory at The Edibles and Infusions Corporation’s (“EIC”) Winnipeg facility, coupled with EIC’s Research License, will also complement the Company’s focus on innovation.

- Per the PDC agreement with BAT, a “Center of Excellence” (or “CoE”) is being established at the Company’s Moncton facility to focus on developing the next generation of cannabis products with an initial focus on CBD. Both companies will contribute scientists, researchers, and product developers to the CoE which is governed by a steering committee consisting of an equal number of senior members from both companies.

- Both Organigram and BAT have access to certain of each other’s intellectual property (“IP”) and, subject to certain limitations, have the right to independently, globally commercialize the products, technologies and IP created by the CoE.

- Approximately $30 million of BAT’s investment in the Company has been reserved for its portion of its funding obligations under a mutually agreed initial budget for the CoE. CoE costs will be funded equally by Organigram and BAT. Currently, the CoE is hiring staff as part of its ramp up.

Outlook

Net Revenue

- Organigram expects Q3 2021 revenue to be higher than Q2 2021 as the Company is improving demand fulfillment with increased staffing. As noted above, the Company’s Moncton facility was shut down during the quarter for deep cleaning after identifying positive COVID-19 cases and a significant number of employees had to isolate. The lost production time resulted in missed revenue opportunities as the Company was unable to fulfill certain demand. Although the Company expects higher net revenue in Q3 2021 due to greater fulfilment rates with increased cultivation and packaging staff, there is the risk that net revenue could be negatively impacted again if there positive cases are identified in the future and the Company needs to take similar measures.. In addition, the COVID-19 restrictions for cannabis retail stores, particularly in the most populous province of Ontario, could suppress demand and negatively impact net revenue in Q3 2021.

- The Company expects to generate more revenue growth from the production of soft chews and other confectionary products with the specialized equipment in the Winnipeg EIC facility. The Company is targeting first sales of soft chews in Q4 2021 subject to certain achievements, including, but not limited to, the timing of receipt and commissioning of certain ancillary equipment, completion of quality assurance documentation, the hiring of requisite staff and obtaining product listings from the provincial boards.

Adjusted Gross Margins

- The yield per plant increased in Q2 2021 from Q1 2021 as a result of optimizing the density of plants per room and decreasing the time spent in vegetation. The higher yield per plant in Q2 2021 drove a lower average cost of cultivation per gram (compared to Q1 2021) such that when this inventory is sold starting in Q3 2021, it will positively impact Q3 2021 adjusted gross margins. However, the overall level of Q3 2021 adjusted gross margins versus Q2 2021 will depend on other factors including, but not limited to, product category and brand sales mix.

- In addition, the Company has identified the following opportunities which it believes have the potential to further improve adjusted gross margins over time:

- The Company expects to gain economies of scale and efficiencies as it continues to scale up cultivation.

- The recent launches of new higher margin dried flower strains under the Edison and Indi brands with more to come in the near term have the potential to positively impact gross margins over time as these products gain traction in the market and comprise a greater proportion of the Company’s overall revenue.

- International sales have historically attracted higher margins and are expected to comprise a greater proportion of the Company’s revenues once the Company resumes shipments to Canndoc (currently expected in Q4 2021 – see International section below).

- The Company is launching more multi-pack pre-rolls and 1g vape cartridges and these higher volume SKUs attract higher margins.

- The Company continues to invest in automation to drive cost efficiencies and reduce dependence on manual labour. For example, the new pre-roll machine was commissioned and began operating in March 2021 which has significantly reduced the Company’s reliance on manual labour.

- As a result of a packaging task force project, a number of cost reduction opportunities have been identified for implementation starting in Q4 2021.

Selling, general and administrative (SG&A) expenses

- Q3 2021 SG&A is expected to be higher than Q2 2021 largely due to increasing staffing related to the BAT and EIC transactions.

International

- The Company continues to serve international markets (including Israel and Australia) from Canada via export permits. The Company is looking to augment sales channels internationally over time. In early Q1 Fiscal 2021, the Israeli Ministry of Health amended its quality standards for imported medical cannabis. The Company is seeking Good Agricultural Practice certification by the Control Union Medical Cannabis Standard and is making progress. Subject to successful completion of a required inspection that is likely to be conducted remotely, the Company currently expects to be certified as early as the end of Q3 2021. Shipments to Canndoc are expected to resume in Q4 2021 contingent upon regulatory approval from Health Canada, including obtaining an export permit, and the availability of the desired product mix.

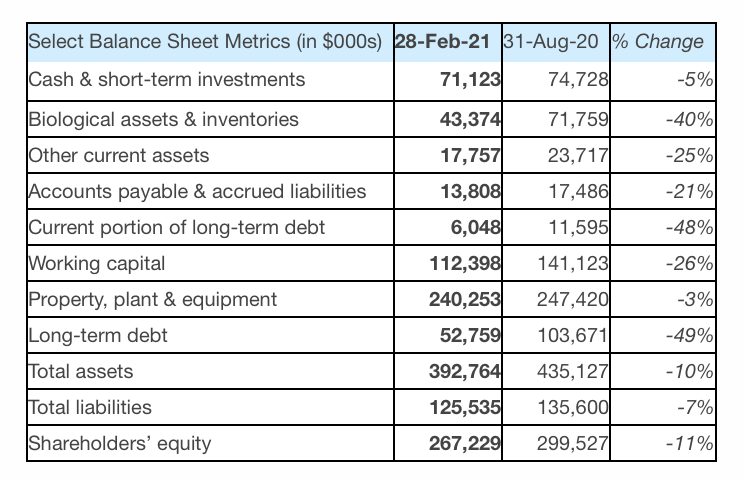

Liquidity and Capital Resources

- On April 1, 2021, the Company repaid all outstanding balances (approximately $58.5 million) under its credit agreement (the “Credit Agreement”) with BMO and a syndicate of lenders which will result in annual interest savings of $2.7 million (based on the outstanding balance at the time of repayment).

- Currently, the Company has $232 million in cash and short-term investments.

- Organigram currently intends to terminate the Credit Agreement and discharge the related security.

Second Quarter Fiscal 2021 Conference Call

The Company will host a conference call to discuss its results with details as follows:

Date: April 13, 2021

Time: 8:00am Eastern Time

To register for the conference call, please use this link:

To ensure you are connected for the full call, we suggest registering a day in advance or at minimum 10 minutes before the start of the call. After registering, a confirmation will be sent through email, including dial in details and unique conference call codes for entry. Registration is open through the live call.

To access the webcast: https://event.on24.com/wcc/r/3079347/ADF4D345BD5DF5386FDEF631BD132518

A replay of the webcast will be available within 24 hours after the conclusion of the call at https://www.organigram.ca/investors and will be archived for a period of 90 days following the call.

Non-IFRS Financial Measures

This news release refers to certain financial performance measures (including adjusted gross margin and adjusted EBITDA) that are not defined by and do not have a standardized meaning under International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. Non-IFRS financial measures are used by management to assess the financial and operational performance of the Company. The Company believes that these non-IFRS financial measures, in addition to conventional measures prepared in accordance with IFRS, enable investors to evaluate the Company’s operating results, underlying performance and prospects in a similar manner to the Company’s management. As there are no standardized methods of calculating these non-IFRS measures, the Company’s approaches may differ from those used by others, and accordingly, the use of these measures may not be directly comparable. Accordingly, these non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Please refer to the Company’s Q2 2021 MD&A for definitions and, in the case of adjusted EBITDA, a reconciliation to IFRS amounts.