This article is the third in a 10 part series on why you should invest in American Multi-State Operators (MSOs) instead of Canadian Licensed Producers (LPs). Consider starting with part 1 here.

I’m not against companies performing secondary stock offerings to buy up the competition if the purchase immediately adds to the company’s bottom line (EBITDA or cash flow), and increases operating efficiencies and margins. What I am against is diluting shareholders through secondary offerings to keep the lights on. This is what separates the U.S MSOs and the Canadian LPs.

Trulieve’s CEO Kim Rivers shows how it’s done in Pennsylvania

On September 16, 2020, Trulieve announced the purchase of two Pennsylvania companies, cannabis wholesaler PurePenn and retailer Solevo who operates three dispensaries. The total cost to enter Pennsylvania was $66 million in cash/stock with $75 million in stock for EBITDA performance incentives. Five days later Trulieve announced a secondary stock offering to raise $90 million to help pay for the deal. Why is this good shareholder dilution?

First, Pennsylvania is the 6th largest U.S. state by population and has one of the fastest-growing cannabis sales in the nation. Additionally, with New Jersey legalizing recreational cannabis use in November, Pennsylvania is racing against New York and Connecticut to be the next northeastern state to fully legalize. Pennsylvania was a must enter state for Trulieve.

Second, these acquisitions are accretive transactions on an EBITDA basis and adds $74 million in revenue on an annualized basis. This transaction is a great example of how U.S. MSOs pay multiples based on 4-6x EBITDA, while most of the Canadian LPs have a history of purchasing properties based on revenue multiples (go look at the staggering Goodwill increases and cash burn rates on the LP financials).

Aurora Cannabis dilutes to keep the lights on

I have a saying, U.S. MSOs sell cannabis, Canadian LPs sell shares to generate cash flow. No one sells shares better than Aurora Cannabis.

As of September 30, 2020, Aurora reported 133.4 million outstanding shares. At first glance that doesn’t seem like a lot of shares, but you factor in that Aurora performed a 12-1 reverse stock split on May 11, 2020 to stay listed on the New York Stock Exchange. That puts Aurora at 1.6 billion shares pre-reverse stock split. Then in November, just 6 months after their 12-1 reverse split, Aurora dumped another $125 million in stock into the market. Why do they dilute so much?

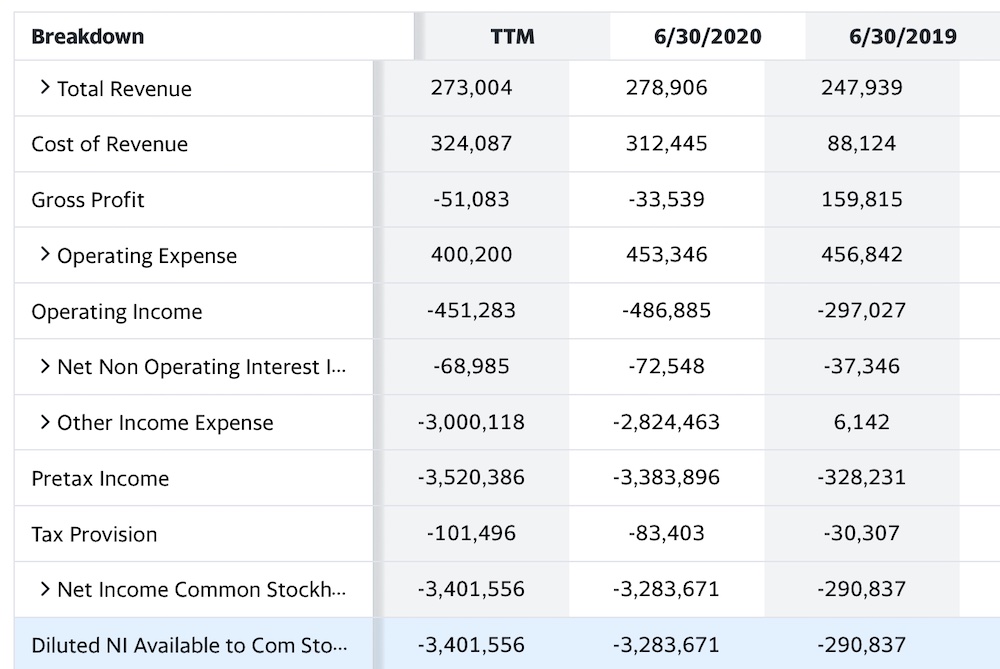

First, Aurora burns through their cash reserves at an alarming rate because their operating losses are so large. For example, their current trailing-twelve month (TTM) loss is at -$451 million.

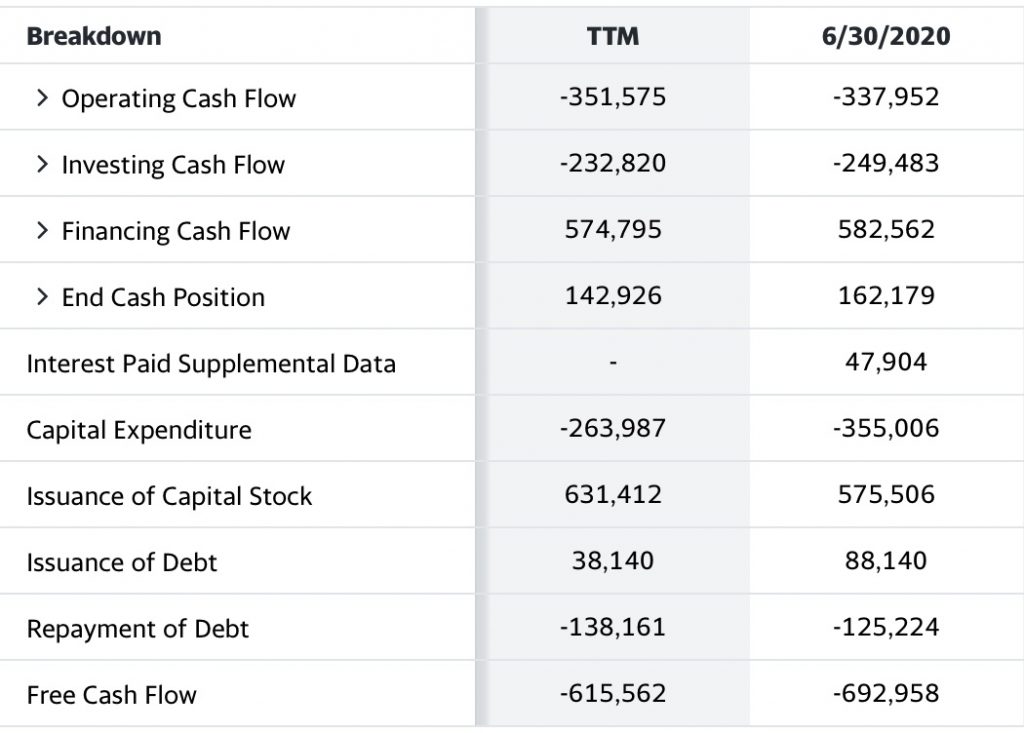

Because of such heavy operating losses and another $164 million in capital expenditures, Aurora had to issue $631 million in new shares. Their free cash flow was -$616 million.

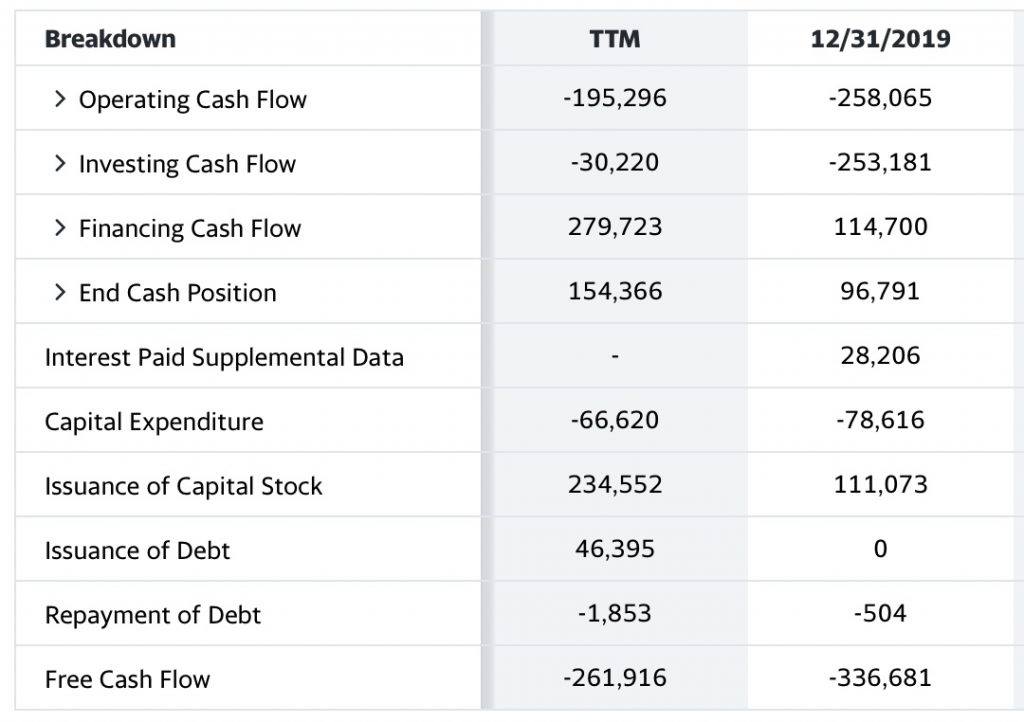

Aurora is not the only extreme example of Canadian companies burning cash and diluting shareholders. Canopy Growth dumped $5.2 billion in shares onto the market, mostly by issuing shares to Constellation Brands who purchased a 38% stake in Canopy in 2018. Canopy has had well over $1 billion in negative cash flow for the past two years now:

When you purchase shares in a company, you are buying a percentage of ownership in that company. When that company issues more shares, you have to purchase more shares just to maintain your percentage ownership or your ownership is diluted. I don’t mind share dilution if the company is adding shareholder value, but I do mind dilution if it’s due to poor management. There is a direct correlation between Aurora’s increased share dilution and lower share price. In 2018, Aurora’s share price hit a high of $129 ($1,548 pre-reverse split) and after a lot of secondary stock offerings pushed the price below $5 in October of 2020. Yes it has bounced back over 100%, but it’s still down 90% from its high. Expect more Aurora dilution soon.

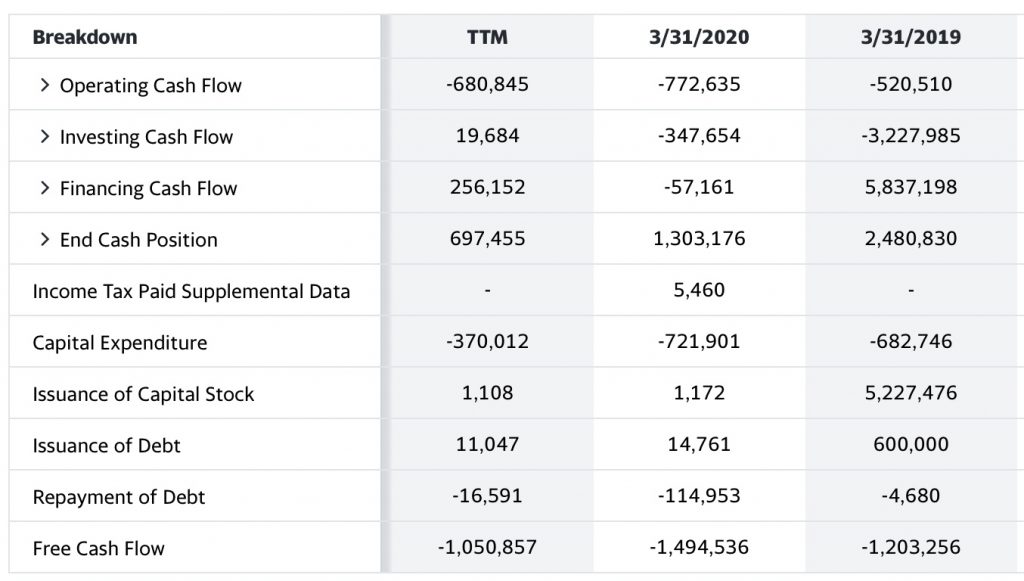

Tilray is pretty much in the same boat issuing $234 million in stock with a free cash flow of -$262 million:

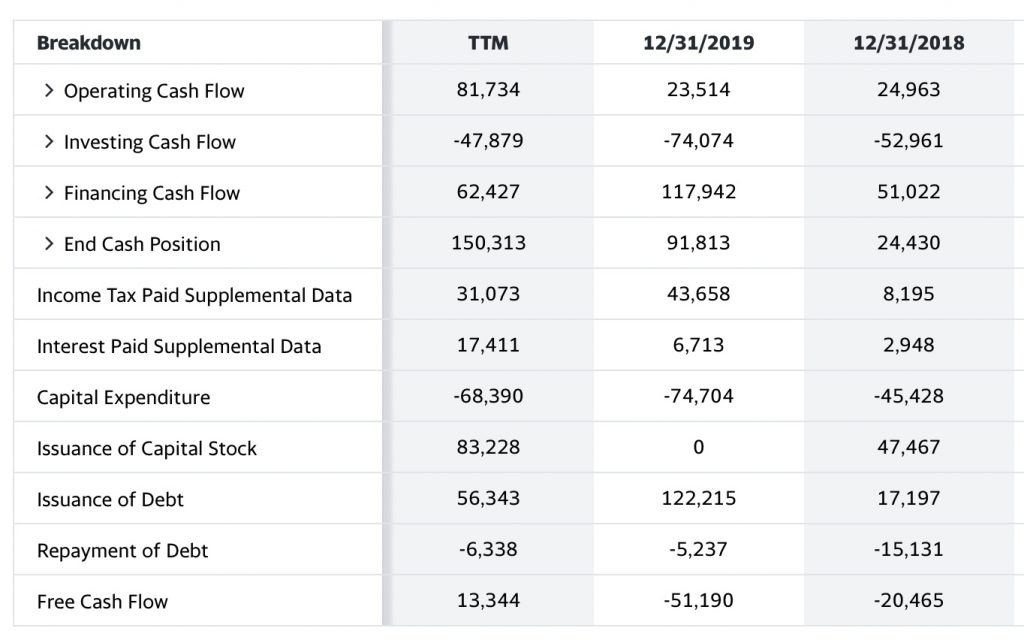

Trulieve is the gold standard when it comes to cash flow and responsible dilution in the cannabis industry – no shareholder dilution in 2019 and only $83 million new shares TTM (the proceeds used for the Pennsylvania acquisition mentioned earlier).

Trulieve’s $13 million in TTM free cash flow doesn’t tell the whole picture as in the last quarter alone they generated a net income of $17.4 million, or $0.15 per diluted share. Not only is Trulieve cash flow positive, the company’s cash flow is accelerating. MSO’s like Trulieve respect shareholders, LP’s like Aurora, Tilray and Canopy do not.

Stay tuned for ‘Reason #4 to invest in American cannabis MSOs over Canadian LPs: Growth.